Our relationship with money, undoubtedly, serves as one of the most defining relationships of our lives.

Whether we hoard it, overspend it, worry about it, chase it, save it, or give it all away, the way we interact and think about money affects countless aspects of our lives.

Some consider money as merely a tool. And that is true, money is a tool.

But it is also much more than that. One must only look at the fact that 77% of people in the richest nation in the world remain anxious about their financial situation to see that money is treated differently in our mind and heart.

And considering that more than 70% of Americans report their desire for money influences their daily decisions, I would again argue stands as proof that money is no ordinary tool. How many people do you know base their daily decisions on passionately acquiring more tools?

Money has a much deeper impact on our lives and psyche than a tool. And we can see it all around us—and inside us.

Therefore, to understand ourselves better and conduct ourselves best, it is essential that we constantly evaluate the role and importance we place on money in our mind and in our heart.

To help, I want to introduce you to a phenomenon concerning money that plays out in a large majority of people’s lives—probably yours and almost certainly mine.

The phenomenon is what I call: The Prosperity Paradox.

This paradox about financial wealth can be summarized this way: The more money we accumulate, the more money we think we need.

And it’s one of the reasons 80% of Americans think they would be happier if they had more money.

Rather than providing happiness and security as many people think it will, money seems to have an opposite effect. The more we have, the more we think we need.

A bold statement, no doubt. One that you probably want to immediately disagree with. But this paradox is not merely a philosophical musing; it is underscored by compelling research and statistics. Let me offer you four studies that clearly display the prosperity paradox in action.

Individuals were recently asked how much money they believed they would need to retire comfortably. The average response was $1.46 million. Numerous articles were written about how that number has increased over recent years.

But read further into the study and you’ll discover a fascinating fact. According to the study, the higher your net worth, the more money you believe you need to retire. In fact, while the average American believes they need $1.46 million to retire comfortably, high-net-worth individuals (people with more than $1 million in investable assets) said they’ll need nearly $4 million to retire comfortably.

The Prosperity Paradox: The more money a person has, the more money they think they need to live a comfortable life.

Here’s another study less focused on the future and more focused on the here and now. Again, we see the same thing happening.

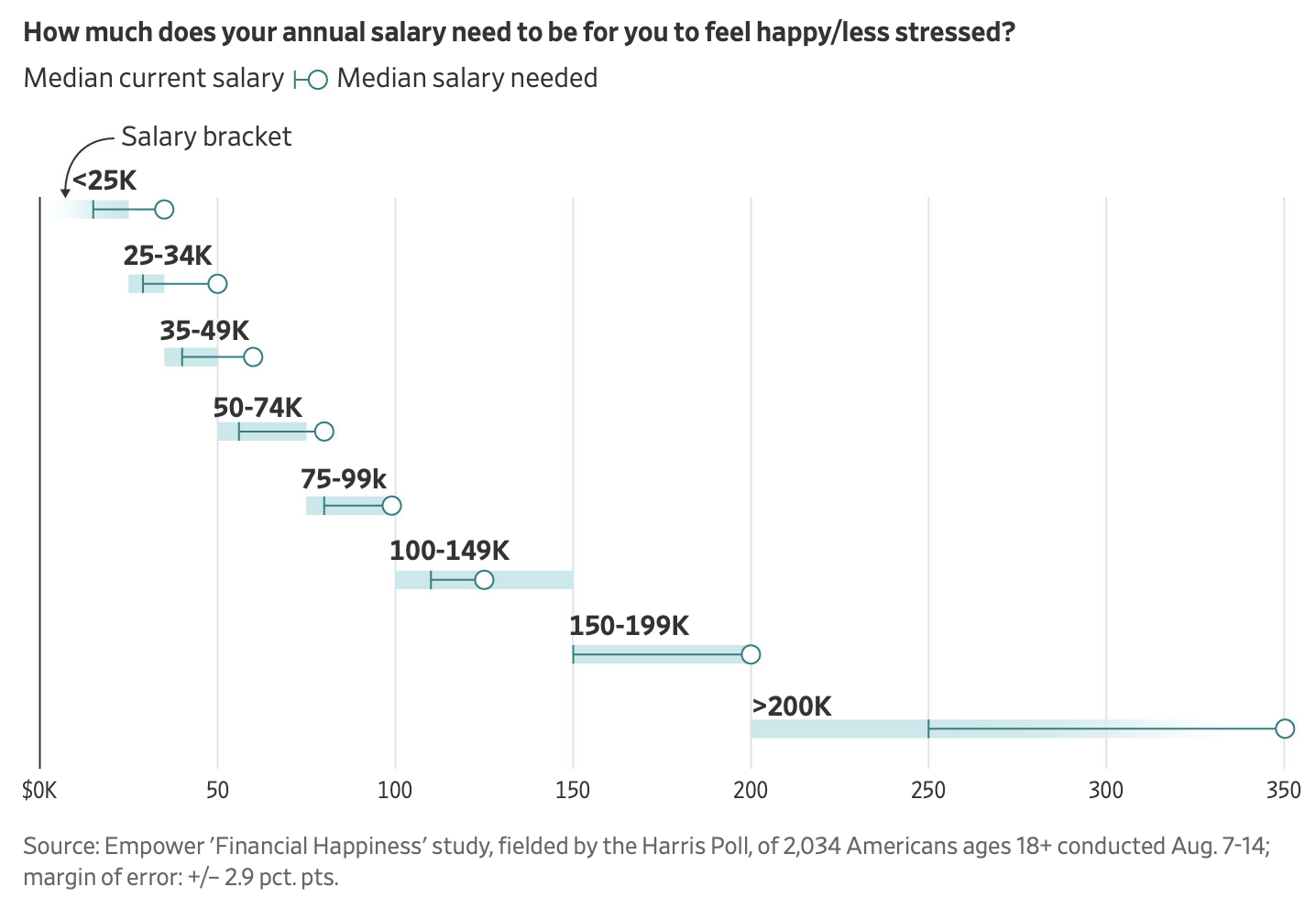

The financial services company, Empower, recently asked people, “How much does your annual salary need to be for you to feel happy or less stressed?”

The median answer to the question was “an additional $30,000/year would result in happiness.” But among the highest earners (those already making more than $200,000/year), they responded that they would need an additional $150,000/year to be happy!

The income brackets align exactly with what the Prosperity Paradox would predict. Across the income brackets, the more money a person makes, the higher the pay increase they said would result in happiness.

You can see the exact breakdown here:

We can also see the paradox in play as to how people define rich.

To many, a millionaire embodies the epitome of financial security. In fact, your specific answer to the question, “Is a millionaire wealthy?” likely reveals quite a bit about your current financial circumstance.

Is a millionaire wealthy?

Did you answer the question, “Yes”? If so, chances are, you don’t have a million dollars. Because the closer you get to that level of net worth, the less likely you are to consider it rich.

In fact, millionaires comprise about 8.8% of the American population. And yet, an astonishing 87% of millionaires do not view themselves as wealthy.

90% of those living in the top 10% of the wealthiest nation of the world do not consider themselves wealthy. How can this be?

Only when you understand the Prosperity Paradox does this self-identification begin to make sense. The more money a person has, the more money they require to feel wealthy. The goal posts of wealth just keep moving further and further away.

But it’s not necessary to only point fingers at millionaires. Did you know that if your net income is $65,000/year, you are among the top 20% of wage earners in the world today?

That’s right, $65,000/year earns you more money than 80% of the planet.

You can run your own numbers here: World Inequality Database.

Is that how you feel earning $65,000/year? Among the very wealthiest in the world? Probably not. Because the Prosperity Paradox rears its ugly head at nearly every income level.

No wonder John D. Rockefeller, the richest man in the world at that time, when asked by a reporter, “How much money is enough?” responded by saying, “Just a little bit more.”

That is the nature of money. It never satisfies. It never brings the happiness we believe it will. It never brings lasting security. Nor does it bring the contentment we desire.

“How much money is enough?” is a question very few people can answer. Except with the response, “Just a little bit more than I have now.”

Be aware. If that is your belief, you will never arrive.

Does anyone have a calculator to help determine what’s enough? My family is saving/investing and I can only hope it will be enough. There’s a lot of variables to consider. Not to long ago, it was recommended to shoot for investing 15% of your salary. Now, a lot of “expert” advisors are saying 20%. I know it’s out of my control. And, I know you can’t put a number on what is enough.

A lot of people recommend the 4% rule as a good guide to follow :)

https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/

Consider your expenses for retirement as opposed to current income. How much will you need per year could be a much lower number if you have minimal expenses and no debt. Twenty five times that is considered “enough” but also take into consideration any income besides investments. Pensions, social security, annuity income, as well as dividends, or other passive sources can all make the “number you need” even less.

I fall into the “wealthy” category after my husband and I saved up for years while leaving below our means. We want to retire early, very early in our forties so our thought process is will this money be enough to last us a lifetime without work while allowing us to do the things we enjoy (travel, be philanthropically) and the things that are necessities (health expenses with age). We want to get off the work train and be comfortable, figuring out what is “enough” and if it will last us gives us the paradox.

living* philanthropic*

My thought. 40 is too Young to Retire.

A brilliant piece, Joshua. It’s so true that, the more we have, the more we think we need. It took me many years to learn the lesson, but I now know that true joy comes from choosing to say no to the message the world constantly sends us, and live a life that aligns with our personal values.

I once owned 38 houses, a 41 foot sailboat, Mercedes, blah…blah…blah. Money has an intrinsic evil that ruins lives.

I think Seneca’s view on money is a good measure on how much we need:

“Where money is concerned, the ideal amount is one that does not fall into poverty and yet is not far removed from poverty.”

“just a little bit more” comes becasue most people spend what they make, so at the end of the month they don’t have the million dollars they made, so of course their perspective says I am not rich. That is because they don’t have enough at the end of the month after expenses. Spend less and you wont need “just a little bit more”

I would like to say, as I’ve learned from other Youtubers, the last moment is in the past, the next monent is in the futue, so it must be that this moment is “enough”.

And if we aren’t content with this moment, we may end up becoming victims of consumerism, which always tries to convince us that “this moment” is not enough for you, me, or anyone else, and that your next monent should include whatever it is that they are trying to sell you.

Thanks for reading this.

Thankfully, I stopped acquiring “stuff” years ago. My house and my car are paid for and, after retirement, I am enjoying a simple life that values experiences. I have traveled to every continent, except Antarctica.

I worked in healthcare and retired at 75 years young and I am grateful every day that my wants do not exceed my means. I have enough.

Lovely reply, Janice. An inspiration.

I do think it’s important to note that an area’s cost of living affects some of this data. But I don’t think that changes my view of the conclusions, which I think is exactly how the author intended them to be.

I feel like it’s important to remember where you came from. Usually when I hear that, it creates a visual of whatever times apply. But in this case, it’s an emotion. When I was in my worst financial times, with the biggest connected stresses, “wealthy” meant “stable”.

Today, I am stable. I’m 50 years old. I still work as a grocery store manager. I’m partnered with someone in a similar profession making similar money. I still have to work and likely will until the traditional retirement age of 65. But we’re on a very solid track to retire on time and do so comfortably. In the meantime, we live humbly and semi-frugally. We don’t quite live a minimalist life (although I advocate for it!). But we don’t live lavishly and do live responsibly. We try not to partake in consumerism and actively save heavily for that retirement. I have almost zero money-related stresses.

The “me” from those toughest of times would consider this “wealthy”.

Money has only one purpose; to buy stuff. It is the physical representation of your sweat called labor.

Money has only one true power; it makes you more of what you already are. A mega million winner will do what with the money if they are an alcoholic? A generous soul? Someone who wants to own stuff that will make his neighbor jealous or think himself successful?

$65,000 is only $45,500 given yearly for me to spend after my government takes what it demands first ( at least in my state). And since I have only nominal control over the prices of things I must buy, living beneath my means gets more challenging every year in the richest nation on earth. But alway, alway, always remember:

DEBT IS A FORM OF SLAVERY

Thanks for the comment Lee Ann. We will have to disagree on this point. Money does not just reveal more of who you are and I’d challenge you to reconsider this commonly-held assumption. Money changes who you are. But that’s a different conversation for a different day.

Thanks for your perspective, Lee Ann.

You: “Money has only one purpose; to buy stuff.” Me: In my mind people may have purposes for things (and that purpose could be referred to as ‘intention’), or they assign a purpose to a thing. Fiat money has no intrinsic value. So, it must be that people assign a value to fiat money, but its value exists insofar as a relation exists between people and the thing (object) bought or sold with a medium of exchange, money.

You: “It is the physical representation of your sweat called labor.” Me: You’re kidding, right? For example, I could do a workout (physical exercise), but I don’t see any relation between my workout and money. How is money related to the sweat from physical exercise? How would I get fiat money from a day, let’s say, at the gym, a day of working out there?

You: “Money has only one true power; it makes you more of what you already are.” Me: That sounds a little bit misleading, and I opine that one of the goals of minimalism is to help people free themselves from errors in thoughts and assumptions. But what power does money have, in and of itself?

But let’s talk for a moment about a possible situation, one that may occur in reality, even though a possible situation posits nothing in reality. Let’s say a $10 bill is upon a dining room table, and a person is standing beside the table. The $10.00 is burned up through fire, and the person standing beside the table drops dead. What is the connection between a ten dollar bill and the person standing beside the table? How did that bill make the person more of what they already were? But let’s say that only the bill is burned up, but the person continues to breathe and stand by the table. Wouldn’t that demonstrate that breathing depends not on the destruction of a ten dollar bill? So what is the connection (or relation) between breathing and a $10 bill?

And here is another question: How does a person’s breathing depend on someone who stops breathing? As far as I can see, it doesn’t.

That said, I’ll conclude this portion of the response with the following quote: “…Take heed and beware of covetousness, for one’s life does not consist in the abundance of the things he possesses.” (Luke 12:15 NKJV) The part: ‘Take heed and beware of covetousness’ is considered a commandment.

Thanks for reading this.

Lee Ann, I agree with your comment, especially the idea that money makes people more of what they already are. I actually think it aligns with the idea of this article. (Maybe Joshua could chime in and explain why he disagrees, if I’m missing something! :)) A generous soul will find a way to be generous even when they don’t have much to share. I don’t think winning the mega millions will make a greedy person generous. In the hands of an addict, well, that money will just buy them more of their substance. We’ve all seen the stories of these tragic downfalls. Someone I love is deeply affected by the Prosperity Paradox and they always tell me that if they won the lottery, they “would help a lot of people.” I do believe that they would continue on the path of over consumption and discontent that they are already on, and it saddens me. I’m considering sharing this article with them, but I’m not sure how well it would be received.

We have a huge gap between our poorest and our richest. People always like to ignore just how desperate the situation is for those at the bottom and instead make blanket statements about how we are the richest country on earth and therefore we all can just fix our financial situations by not spending it on frivolities. Those statements are harmful to any progress to making social changes towards improving the lives of those who can’t or can barely afford the bare necessities needed to survive. Maybe Josh’s blog is only intended for those comfortably in the middle class and above, because he always ignores the existence of people in this situation and instead keeps making these misleading posts. Having been I’m that situation I can assure you that food, housing, and toiletries, things that someone who is already spending the least they can on those, and a bit more money would actually improve their lives.

I agree with this up to a point. Cost of living must be taken into account. This was firmly realized for my family when teenaged Cuban visitors were stunned to hear about mortgage payments and utility costs and their choices to spend on snacks and souvenirs that my kids would not consider buying.

Joshua, again, such a thought-provoking, well- written article…thank you! It’s spot on. What really is enough? $65K seems like a solid amount to live on. Our U.S. inflation rate of typically 2-3% as been so relatively stable compared to other countries, but now, we all know that most everything has gone up in price and often substantially. Though some got raises, it still doesn’t cover it all. But your point is…when will we be content with ENOUGH? Will we always have the mindset “I need just a little more.” My dad turns 101, God willing, in June. A Great Depression guy. HIs mindset, passed on the the next generations, have produced an incredible work ethic in me and my siblings and our children and grandchildren. HOwever, as I see it play out, my extended family isn’t all that generous though most of us have “more than enough”. The discontentment carries on, sad but tru.

If I take that $65k to another place with a different cost of living, I can live comfortably. But I am here in NJ, where the cost of living is one of the highest in the US if not the entire planet, and I am adjusting my dreams to fit my income. I realize I have student loans instead of a mortgage, and I pray my health stays good, and I

try to squeeze as much living as I can into each day. It’s difficult to accept that some things I grew up thinking were givens may be out of reach for me. And that’s when I need to dig deep and be grateful for where I am, who I am, and the life that I am living without sinking into grieving over what I thought was going to happen or what I thought I was going to have.

We all need gratitude for what we have and focus on the blessings of what we already have. I think this is what “save” us of only want more and more, being mindful of what we already possess.

I understand and believe in your point. However, as Mark Twain famously said, “There are 3 kinds of lies: lies, damned lies, and statistics.” Statistics taken out of context can mean anything — and the one about a $65K salary is a good example. Yes, that salary is more than 80% of what’s earned worldwide — however, that salary is earned here in the US, where the earner lives, and where it’s not enough to buy a house, pay off student loans, own the car that is necessary to get to the job, buy food, etc. That $66K salary puts the earner squarely into the US middle class.

Bette, I definitely agree with this! We are a primarily one income household, and although we make a little bit more than the $65k average annually, just grocery costs for our family of 4 eat 20% of our take home pay. I love the sentiment of the article, but my $65k does not go as far as it would in a lower cost area.

I had the good fortune of taking Dr. Maria Nemeth’s The Energy of Money course in 2001. I still refer to her book, The Energy of Money: A Spiritual Guide to Financial and Personal Fulfillment often. Money is truly one of the energies, when studied, that can offer so much information about how one shows up in life. Like all things, knowledge used and aligned with intentional goals is power to live more abundantly. And that could actually be with less $ versus more. Or not. Fits right in with minimalism – waking up and living with intention.

Per the inequity survey, even though I have quite a low income, because I don’t own a home and it’s just me it seems I’m in the top 40% in the US and to 10% in the world with my salary…. That was quite eye opening!!

Eye opening article. I definitely agree and hopefully will learn from this- to be very happy with what I have and enjoy life

“Of all the things that mean a lot, money’s not.

But if anything will help a little, it’ll.”

Have an awesome day!

The neoliberal capitalist system does everything to make each of us believe we can all live like Kings. The moment you adhere to that idea you become its servant.

Spot on, JF.

The sooner one knows that is blatantly false, the sooner one can be satisfied and content.